Imagine a typical morning in Nairobi, Kampala, or Dar es Salaam. A small shop owner wakes up to a text message notification. It’s not just a greeting; it’s a payment confirmation from a customer who bought goods last night. She uses her simple feature phone to pay her supplier for today’s stock. Later, she sends a portion of her earnings to her mother in a rural village, who receives it instantly and pays for her grandchild’s school fees. No bank branch was visited. No thick wallet of cash was carried through risky streets. This seamless, digital rhythm of finance is the daily reality for millions in East Africa, powered by a revolutionary technology: Mobile Money.

What Exactly is Mobile Money?

At its core, mobile money is a digital wallet stored on your mobile phone. It allows you to send, receive, and store money using a simple SIM card and a basic handset—no smartphone or bank account is required. Think of it as your phone becoming a personal bank branch, open 24/7, in your pocket.

This system has fundamentally revolutionized finance for millions in East Africa. It has turned every mobile phone into a tool for economic participation, bringing financial services to millions who were previously excluded from the formal banking system.

1: The Mobile Money Revolution: A Brief History

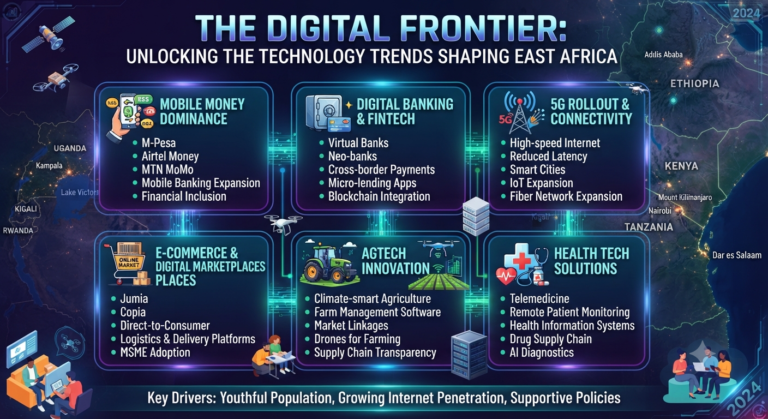

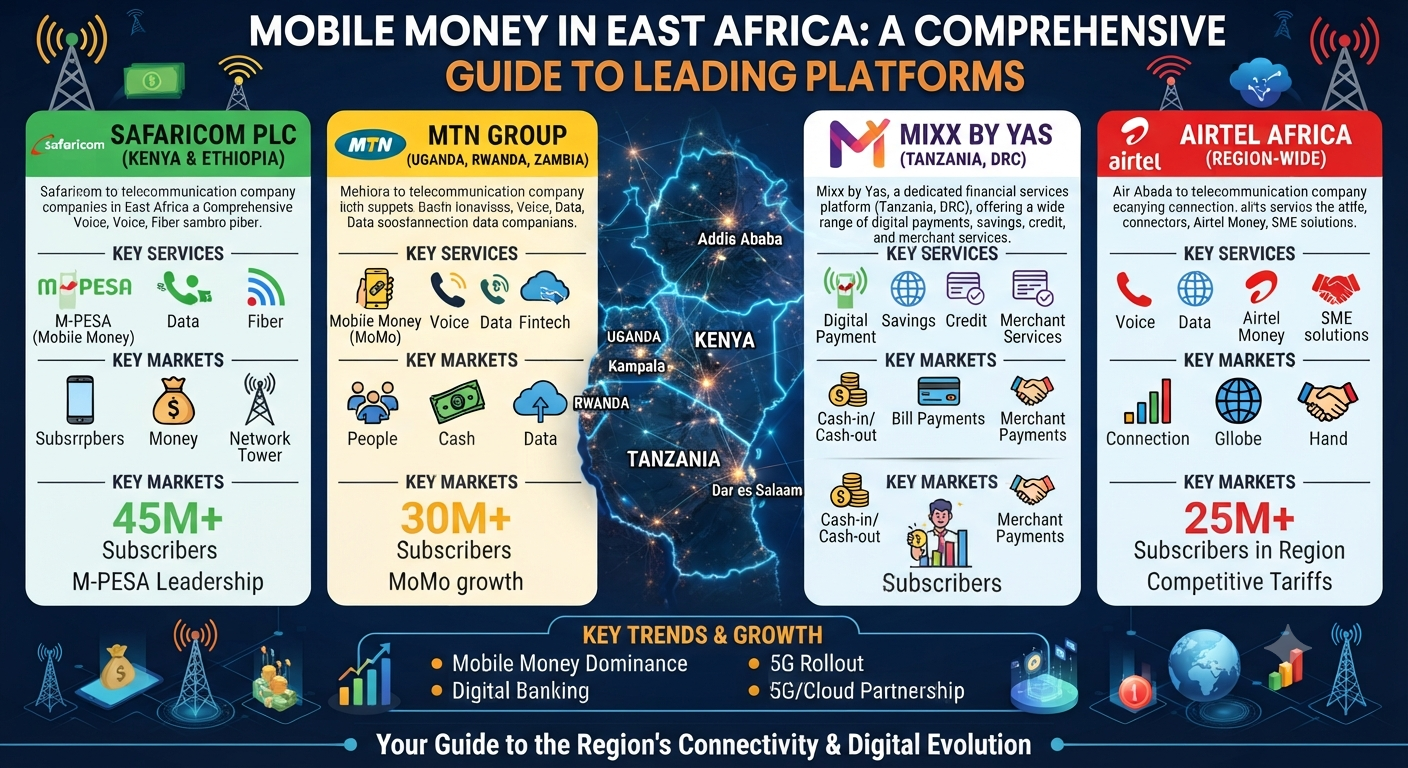

The story of mobile money in East Africa begins with one groundbreaking service: M-Pesa in Kenya. Launched in 2007 by Safaricom, “M-Pesa” translates to “Mobile Money” (M for mobile, Pesa for money in Swahili). It was initially designed to help microfinance institutions disburse and collect small loans. However, Safaricom soon realized its potential for person-to-person (P2P) money transfers, allowing urban workers to send money home to their families instantly.

This simple concept ignited an explosion. Several key factors drove its rapid adoption and spread across the region:

- Solving a Real Problem: It addressed the high cost, inconvenience, and danger of physically transporting cash between cities and rural areas.

- Agent Network: Instead of ATMs, Safaricom built a vast network of local shopkeepers as “agents” who could exchange cash for digital credit and vice versa. This made access easy in every neighborhood and village.

- High Mobile Penetration: East Africa already had high mobile phone ownership, even among low-income populations. Mobile money piggybacked on this existing infrastructure.

- Trust and Ease of Use: The system was designed for simplicity, using SMS/USSD codes (like

*123#) that worked on any phone.

The success in Kenya was a template. Soon, similar services launched across the region, tailored to local markets.

2: How Mobile Money Works: The Basics

Using mobile money is simpler than you might think. Here’s a step-by-step breakdown:

- Registration: You visit a licensed mobile money agent (a local shop with the provider’s signage). You bring your phone and identification (like an ID card). The agent will help you register your phone number and set up your mobile money account.

- Getting Started (Top-up): You give the agent physical cash (e.g., $10). They will “load” or top up this amount into your digital wallet. You receive a confirmation SMS.

- Using the Service: You can now use the menu on your phone (often via a USSD short code) to:

- Send money to another registered user’s phone number.

- Pay bills directly to companies (like electricity, water, or TV providers).

- Buy goods by paying merchants.

- Withdraw cash by visiting an agent and providing your PIN (Personal Identification Number).

- Security: Every transaction requires your secret PIN. This ensures that even if you lose your phone, no one can access your money without it.

Key Terms to Know:

- Agent: A licensed retailer who provides cash-in and cash-out services.

- Wallet: Your mobile money account where digital currency is stored.

- PIN: Your secret password for authorizing transactions.

- Top-up: Adding physical cash to your digital wallet.

- Withdrawal: Converting digital money back into physical cash via an agent.

3: The Undisputed Leader: M-Pesa

M-Pesa, operated by Safaricom (a Kenyan company), is not just a service; it’s a phenomenon and the undisputed leader.

- Origins and Dominance: Born in Kenya, it quickly achieved massive penetration. In Tanzania, through a partnership with Vodacom, it became equally dominant, known simply as M-Pesa. In both countries, it is not just a payment system but the de facto backbone of the digital economy.

- Key to Success: Its success lies in its first-mover advantage, a meticulously built agent network (which has become a source of income for hundreds of thousands), and continuous innovation. It became the trusted utility for money.

- Expansion and Influence: M-Pesa’s model has been studied and adapted globally. While its direct expansion is focused on its core East African markets, its influence is everywhere. It set the standard, proving that a telco-led financial service could be more accessible and agile than traditional banking.

4: Other Major Players: The Competitive Landscape

While M-Pesa leads, the market is competitive, with strong regional players offering viable alternatives.

- Airtel Money: Operated by telecom giant Bharti Airtel, this service is a major contender, especially in Kenya, Uganda, and Tanzania. Its key strengths are its competitive pricing (often offering lower transaction fees for transfers) and aggressive marketing. Following mergers in some markets, it has absorbed other services like Tigo Pesa.

- MTN Mobile Money (MoMo): The flagship financial service of MTN Group, this platform is the dominant force in Uganda and Rwanda. Known simply as “MoMo,” it boasts a massive user base in these countries and is also present in Ghana, Cameroon, and beyond. It’s deeply integrated into the daily commerce of its core markets.

- Tigo Pesa (now Mixx by Yas): Launched by Millicom (Tigo), this service was popular in Tanzania, Rwanda, and Ghana. In several markets, including Tanzania, it has been merged with Airtel Money to create a stronger competitor to M-Pesa, pooling resources and subscribers.

5: How to Choose a Platform: Key Features to Compare

Choosing between M-Pesa, Airtel Money, and MTN MoMo depends on your personal needs and location. Here’s what to compare:

- Network Coverage: This is the most critical factor. Which service has a strong agent network and reliable service in your specific town, village, or neighborhood? An agent nearby is essential for cash-in/out.

- Transaction Fees: Fees vary between providers and for different transaction types (sending money, withdrawing, paying bills). Compare the tariffs for your most common transactions. Sometimes, the cheapest option isn’t the most convenient.

- Ease of Use & Customer Support: How intuitive is the menu system? How easy is it to resolve issues? Check reviews or ask friends about their experience with customer service hotlines and agent professionalism.

- Extra Services: Do you need more than basic P2P transfers? Compare the range of value-added services like:

- Micro-loans (e.g., M-Pesa’s Fuliza, Airtel’s Tingg Loans).

- Savings products (e.g., M-Pesa’s M-Shwari with KCB Bank).

- Bill payment and merchant payment options.

6: Beyond Sending Cash: The Ecosystem of Services

Modern mobile money is far more than a digital cash transfer service. It has evolved into a comprehensive financial ecosystem.

- Payments: The core utility. Pay electricity, water, and DStv bills. Buy goods from supermarkets and local dukas (shops) by simply entering the merchant’s till number.

- Savings and Credit: This is a game-changer. Platforms partner with banks and micro-lenders to offer:

- Micro-Loans: Instant, short-term loans approved based on your transaction history, disbursed directly to your wallet (e.g., M-Shwari, KCB M-Pesa).

- Savings Tools: Earn interest on money saved in your mobile wallet, encouraging a culture of saving.

- International Remittances: Receiving money from family abroad is now easier. Services like WorldRemit and Remitly partner with local mobile money providers, allowing diaspora funds to be deposited directly into a recipient’s mobile wallet.

7: The Benefits: Why It’s a Game-Changer

The impact of mobile money on East Africa cannot be overstated. It is a true game-changer because:

- Financial Inclusion: It brought millions of unbanked and underbanked people into the formal financial system, giving them access to credit, savings, and a secure way to manage money.

- Safety and Security: Carrying large amounts of physical cash is risky. Mobile money reduces this risk. Your funds are stored digitally and protected by a PIN.

- Unmatched Convenience: Financial services are available anytime, anywhere—at home, at work, or on the go. No more traveling to a bank branch during limited hours and waiting in long queues.

- Economic Empowerment: It has created opportunities for small businesses, enabled micro-entrepreneurship, and made the movement of money faster and cheaper, stimulating local economies.

8: Challenges and What to Watch Out For

Despite its benefits, mobile money is not without its challenges:

- Transaction Limits and Costs: Daily transaction limits and fees for cash withdrawals can be a hurdle for users needing to move large sums frequently.

- Network and Technical Issues: Service downtime, network congestion, or lost transactions can occur, causing frustration. Always ensure you have a stable connection before initiating a key transaction.

- Fraud and Scams: This is the biggest risk. Be vigilant against:

- Phishing: Fake calls or messages pretending to be customer support asking for your PIN.

- “Wrong Number” Scams: Someone sends you money by “mistake” and then asks you to send it back, but the initial payment was made with a fraudulent instrument that later gets reversed.

- Agent Fraud: In rare cases, corrupt agents may attempt to shortchange you.

9: Security Tips for Users

Protecting your mobile money is as important as protecting your physical cash.

- Guard Your PIN: Never share it with anyone, not even with an agent. Treat it like your bank PIN. Change it regularly.

- Recognize Scams: Never send money to a stranger. Legitimate companies will never ask for your PIN over the phone or SMS. Delete suspicious messages immediately.

- Lost or Stolen Phone:

- Immediately call your mobile money provider’s customer care number to block your wallet and SIM.

- File a report with the police.

- If possible, use another phone or the provider’s app to log in and deactivate the service.

- Check Your Balance Regularly: Monitor your transaction history via SMS alerts or the provider’s app to spot any unauthorized activity quickly.

10: The Future of Mobile Money in East Africa

The mobile money revolution is still evolving. Here’s what the future holds:

- The Rise of “Super-Apps”: Platforms are transforming into all-in-one ecosystems. The M-Pesa app, for instance, is integrating e-commerce, ticket booking, and more. The goal is to become your single app for commerce, finance, and daily life.

- New Technologies and Interoperability: We are seeing more interoperability—allowing you to send money seamlessly from M-Pesa to Airtel Money or MTN MoMo. The introduction of QR code payments and deeper integration with banking systems are accelerating.

- Innovations in Lending and Insurance: Expect more sophisticated credit scoring based on mobile money data, leading to fairer loans. Micro-insurance products (health, crop, funeral) will become more widespread and easier to purchase via mobile money.

- Regulation: Governments are creating clearer regulatory frameworks to foster innovation while protecting consumers and ensuring financial stability.

Conclusion

Mobile money in East Africa is more than a financial product; it is a social and economic catalyst. From the humble beginnings of M-Pesa in Kenya to the diverse competitive landscape today, it has fundamentally redefined how millions save, spend, share, and invest. It has built bridges between the banked and unbanked, the urban and the rural, creating a more inclusive financial future.

As you navigate this digital economy, remember to embrace the convenience and opportunity it offers, but do so with awareness and caution. Secure your PIN, stay informed about scams, and choose the platform that best fits your life. The power to manage your finances is now, quite literally, in your hands.

FAQ Section

Q1: Do I need a bank account to use mobile money? A: No. This is the greatest strength of mobile money. You only need a valid ID to register with an agent. Your money is stored in your mobile wallet, not a traditional bank account.

Q2: Can I use mobile money without internet (Wi-Fi or data)? A: Yes. The core services (sending money, paying bills) are typically accessed via USSD codes (like *123#), which work on any mobile phone network without needing internet data. However, using the provider’s smartphone app will require data or Wi-Fi.

Q3: What happens if I send money to the wrong number? A: This is a common mistake. Act immediately. Contact your mobile money provider’s customer service with the transaction details (date, time, amount, wrong number). They may be able to reverse the transaction or help contact the recipient, especially for larger amounts. Prevention is key: always double-check the recipient’s number before confirming.

Q4: Are mobile money transactions secure? A: Transactions are very secure when you follow basic safety rules. Your account is protected by a PIN. The main risks come from sharing your PIN with others or falling victim to scams. Always keep your PIN confidential.

Q5: Can I use mobile money to shop online? A: Yes. Many e-commerce websites and apps in East Africa accept mobile money as a payment method at checkout. You simply choose “Mobile Money” as your payment option and follow the prompts on your phone to authorize the payment.